Nickel: The World's Most Hated Commodity, and 60% Of The Case Resources Portfolio

Widespread Perceptions Of Chronic Oversupply Does Not Reflect Reality

Recently, I was watching an episode of the Money of Mine podcast, an Australian natural resource investing show, which I watch religiously. This particular episode was a compilation of thirty natural resource investment manager interviews. Amongst several other questions, each of them were asked:

What do you think the worst performing commodity in 2026 will be?

The consensus is clear - Nickel is the most hated commodity amongst investment managers. The phrases “Nickel is a dog” and “Western Nickel assets are un-investable” were thrown around several times. Poor Nickel can’t seem to get a win, it seems.

I watched this podcast with my brokerage account open on my other monitor, and it made me smile. Why? Because I know that the best way to make money in natural resources is hate - specifically, buying into hated commodities, which won’t be hated in 1-3 years from now. As Rick Rule would say, “I love hate”.

Today, I could not be happier, as Nickel assets sit at approximately 60% of the Case Resources portfolio. I believe that Nickel supply has been grossly over-estimated because quite frankly, most analysts are too lazy to dig deep into the numbers. Once you peel back the curtain, the narrative that Nickel is grossly oversupplied does not hold up to scrutiny. A combination of overstated oversupply, a near-term catalyst for it to become fairly stated, and incentives for the worlds’ largest Nickel producer to raise prices, are setting Nickel up for an explosive turnaround.

Let’s dig into it. Subscribe, for 100% free, to be the first to hear about high conviction investment ideas every week, and to support my work.

The Phantom Surplus

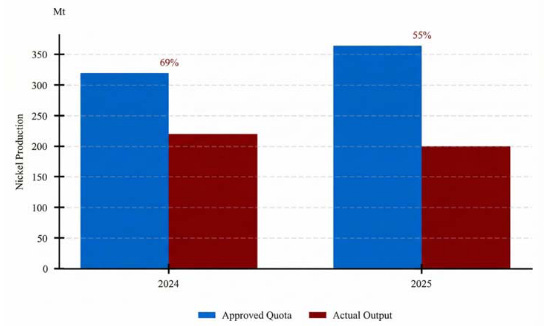

The Indonesian government approved production quotas totalling ~360 million tons for 2025. However, according to the Indonesian Nickel Miners Associated, actual production only translates to a measly utilisation rate of 50-60%. This follows a similar pattern as 2024, where the Indonesian government set quotas for 320 million tons of production, but only actually produced 220 million tons.

Largely, the market is pricing Nickel based off Indonesia’s stated quotas, causing overestimations of nearly 50%. The habit of sell-side analysts to use Indonesian government quota figures is a massive driver of the consensus opinion we’ve seen amongst investment managers.

The reason for oversupply is simple - a new quota system, implemented in 2023, has created perverse incentives of speculation. Prior to 2023, Indonesia operated an annual quota approval system. Then, the system was restructured into a three-year system. The result was that mining companies have begun submitting extremely large quota requests, in a speculation that the Nickel price would rise. The idea is that they would request a large production quota, and then under-produce in years 1 and 2, in the hopes that Nickel prices would be more favourable by year 3, so they could then capitalise by selling more at higher prices.

Today, industry estimates suggest that ~150 million tons of quota capacity represents speculation.

Figure 1: Indonesian Nickel Ore: Approved Quota vs. Actual Output

The impacts of this cannot be understated. Mining companies, sell-side analysts, and investors almost always rely on the International Nickel Study Group for supply-demand estimates. However, INSG data has seen divergences from reality since 2021, and today are just plain wrong.

In 2025, the INSG reported a surplus of approximately 450,000 tons. Yet the actual increase in global market inventories over the same period was only 150,000 tons, a 200% divergence. Whilst some Nickel trading occurs off-exchange, the vast majority of this divergence is down to poor data quality issues. Whatever the cause, analysts relying on INSG data are over-estimating the degree of global over-supply by 150-200%.

Importantly, there is a catalyst for a reversal of these over-estimates. On January 1st 2026, Indonesia will be reverting to their annual quota system. This change should meaningfully reduce the supply forecasts of the majority of sell-siders, whom rely on Indonesian quota data for their forecasts.

Show Me The Incentive, I’ll Show You The Outcome

Let’s first address the elephant in the room properly: Indonesia controls the Nickel market. Producing over 60% of the world’s supply, they have a strong capacity to set prices at rates they see fit, above their producers price floors.

Prior to April 2025, Indonesia levied a flat 10% gross value tax on Nickel ore, regardless of price. The revised system has shifted to an ad valorem tax with price-indexed rates. Nickel ore rates now range from 14-19% dependent on price, with intermediate rates scaling continuously.

This creates a clear fiscal incentive for the Indonesian government to raise the Nickel price. Under the new regime, Every $1,000/t increase in Nickel prices directly translates to $250/t of additional tax revenue. To put this into perspective, $20,000/t Nickel would now lead to 55% greater tax revenues, in comparison to $15,000/t. Under the old system, it would have been ~30%.

The Sentiment Shift

So, we have a single country which has the capacity to raise the Nickel price at will, and now has a much stronger incentive to do so. In addition, there is a strong catalyst in place for analysts to recognise that existing over-supply has been vastly overstated. This, in addition to the existing structural factors which lead to higher commodity prices over time (finite supplies and ore grade deterioration), is setting the Nickel market up for an explosive 2026.

These factors are just the fundamentals. In a rational market, this would be the end of my write up. However, as we know, there is a powerful behavioural angle in commodities. In no way is the behavioural factor more powerful than when you are looking at something which hated and/or unloved. Nickel is the hated commodity right now, rivalled only perhaps by Oil & Gas.

The sharper analysts, who recognise the factors I’ve outlined here, are forecasting prices of $18,000/t by the end of 2026, based on fundamentals alone. When you add the speculation and emotional response to rising, I can easily foresee prices of above $20,000/t within the next 12 months.

The Best Way to Play the 2026 Nickel Boom

I have several positions, but by far the largest is Canada Nickel Company Inc. (TSXV:CNC), at ~50% of the Case Resources portfolio. CNC’s Crawford project is expected to go into construction in third quarter of 2026. At a U.S. $2.8b NAV(8%), a 41 year mine life, and life of mine AISC of $1.54/lb Ni, the project boasts excellent economics and can feasibly go into production at the current Nickel price.

The company is expecting to receive several hundred million dollars of government grants, to fund a portion of project Capex. Canadian Prime Minister Mark Carney has even gone as far to saying that Crawford is “the future of Canada”.

Beyond Crawford, Canada Nickel has a footprint of Nickel projects 17x Crawford’s size, all sitting around the Timmins camp. The company is planning to build one of the largest industrial clusters in the world, with Nickel mining, downstream processing, stainless steel manufacturing, C02 sequestration, and potentially even Hydrogen/Ammonia production, all within a concentrated area.

My price target remains at C$8 within 12-24 months. The stock trades at ~C$1.20 now, I am very confident to have have the stock at such a large percentage of my portfolio. You can read my latest report on the stock here:

Appreciate your work and bringing this company to my attention. I doubled down on CNC last night after a month or so of stale performance after the breakout. Was happy to wake up to an announcement this morning.

Doesn't it bother you that Crawford is extremely low grade deposit? Also have you looked on Magna Mining?