Bunker Hill Mining Corp. (TSXV:BNKR) - A 55% Upside, Unfollowed Mine Restart Story - Production By April 2026

At 80% IRR, Bunker Hill Shares Offer An Attractive Risk/Reward Profile

Share Data

Recommendation: BUY Symbol: TSXV:BNKR

Sector: Metals & Mining Last Close: C$0.22

12-month Target: C$C0.34 Target Return: 55%

P/NAV (10%): 0.73x 52-Week Range: C$0.095 - C$0.27

Analyst Targets: C$0.25

Summary

At its simplest, investing comes down to one simple challenge: how can I maximise my annualised returns whilst taking the minimum amount of risk?

Note: when I say risk, I make no reference whatsoever to how professional financiers would define it - volatility. I refer to what risk actually is - the probability of a permanent capital loss.

In the right situations, “last-mile” junior miners, i.e. projects already under construction, can offer some of the best risk-return trade-offs in the business. Yes, you will likely never hit a 10-bagger on one of these names. But, you may achieve 50% or 100% over the space of a year, taking relatively little risk in the process.

I believe Bunker Hill to be one of these names - a low capex, multi-commodity mine restart currently being executed by an excellent management team, supported by Teck Resources - one of the largest mining corporations in the world. Teck has taken a ~32% stake in the business, with a simple incentive - they need a mine to feed their nearby smelter, as their current mine comes off-line imminently. Teck and Bunker hill have agreed a Life of Mine off-take agreement for 100% of the Lead and Zinc concentrate produced on site.

Production is ~3/4 complete, procurement is ~100% complete, and the off-take agreement has secured future sales. These three factors provide a meaningful reduction in risk - with ~55% upside to current NAV + cash + salvage value. In addition, I believe the Bunker Hill asset package has significant exploration upside, which isn’t price in to my valuation. There are multiple catalysts over the next 12 months which should cause this value to be realised. As such, I initiate coverage on $BNKR.V as a position in the Case Resources portfolio, at ~5% of total capital.

History of the Bunker Hill Project

The Bunker Hill Mine in Kellogg, Idaho, was one of the most significant lead-zinc-silver mining operations in American history, operating for approximately 95 years in the Coeur d’Alene mining district.

Phillip O’Rourke filed the original Bunker Hill mining claim on 10 September 1885, naming it after the Revolutionary War battle. The famous discovery involved Noah Kellogg, whose jackass reportedly led prospectors to the galena ore vein. Simeon Reed purchased the mine and incorporated the Bunker Hill and Sullivan Mining and Concentrating Company on 29 July 1887. Operations scaled rapidly: by 1891, the Old South Mill processed 150 tons of ore daily, and a 10,000-foot aerial tramway connected the mine adit in Wardner to the mill in Kellogg. The company completed the 12,000-foot Kellogg tunnel in 1903 and began operating its own smelter at Smelterville on 5 July 1917.

By the late 1940s, the mill processed 3,000 tons of ore daily, while the smelter produced nearly 10,000 tons of lead monthly. Discovery of the massive Shea ore body in 1949 extended the mine’s reserves significantly. At its peak, the operation produced approximately one-third of the nation’s lead, half its silver, and over one quarter of its zinc.

Gulf Resources & Chemical Corporation acquired Bunker Hill in 1968 and operated until announcing closure in August 1981, citing low metal prices and stricter EPA air quality regulations. When the smelter closed in December 1981, it was the world’s largest lead smelter, employing 2,100 workers. The mine briefly reopened in 1988 before final closure in 1991.

Over its operational life, Bunker Hill produced approximately 42.77 million tonnes of ore averaging 8.43% lead, 4.52% zinc, and 3.52 ounces of silver per ton, yielding an estimated 165 million ounces of silver. Today, Bunker Hill Mining Corp. is pursuing a restart of mining operations, targeting production by 2026. BNKR is the 100% owner of the project.

Infrastructure & Access

The Bunker Hill mine project is conveniently situated 60 miles east of Spokane, Washington, accessible via Interstate 90 to the mile 50 exit, with proximity to regional aviation hubs at Spokane (60 miles west) and Missoula, Montana (125 miles east). The underground workings are reached through the 10,000-foot Kellogg Tunnel at the 9 Level elevation, accessed via the public McKinley Avenue and Bunker Mine Road. Positioned at ~2,300 feet above sea level, the property benefits from a climate suitable for year-round mining activities. Rail infrastructure provides direct connectivity to both the Kellogg portal and primary mine yard. The Avista Kellogg substation, situated adjacent to Bunker Hill’s main offices, delivers power supply to the mine and surrounding regional consumers. Existing surface and underground infrastructure encompasses water management systems, drainage facilities, and an engineered hydraulic backfill plant. Substantially all underground development and infrastructure remains operational at the Bunker Hill complex, while reclamation efforts have addressed the former mill, smelter, and tailings impoundment sites.

Geology

The Bunker Hill property occupies the Northern Idaho Panhandle, underlain by Middle Proterozoic Belt-Purcell Supergroup fine-grained siliciclastic sedimentary rocks. Economic mineralization concentrates within the Upper Revett formation of the Ravalli Group.

The deposit comprises four primary mineralization styles. Bluebird Veins exhibit west-northwest striking geometries with southwest dips, characterized by variable sphalerite-pyrite-siderite assemblages with gradational margins along bedding and fractures. Stringer and disseminated zones represent fracture and bedding-controlled sulfide blebs associated with Bluebird structures. Galena-Quartz Veins display east to northeast strikes and south to southeast dips, consisting of quartz-argentiferous galena with siderite, sphalerite, chalcopyrite, and tetrahedrite, cross-cutting Bluebird Veins with sharp boundaries. Hybrid zones develop where Galena-Quartz Veins intersect Bluebird Veins, featuring open-space sulfide and quartz deposition within quartzite beds.

Quartzite units of the Revett formation host all vein types, with mineralization concentrated in open-space fractures created by vein refraction transitioning from softer siltite-argillite into quartzite lithologies. Alteration patterns lack the pronounced zonation typical of porphyry copper or epithermal deposits, though disseminated sulfides and siderite halos surround both vein types. While Bunker Hill shares similarities with neighboring Coeur d’Alene operations such as Sunshine, Crescent, and Galena mines, its distinctive structural controls and mineralogy likely represent a discrete component of broader district-wide zonation patterns.

Bunker Hill - Project Economics & Valuation

The Bunker Hill mine underground mine restart is to come in two phases:

An initial ramp up to 1,800 tpd milling capacity, with a 5 year mine life

Bunker 2.0: an expansion to 2,500 tpd milling capacity, and a 15 year mine life, through a U.S. $60m capital investment to expand the existing mine.

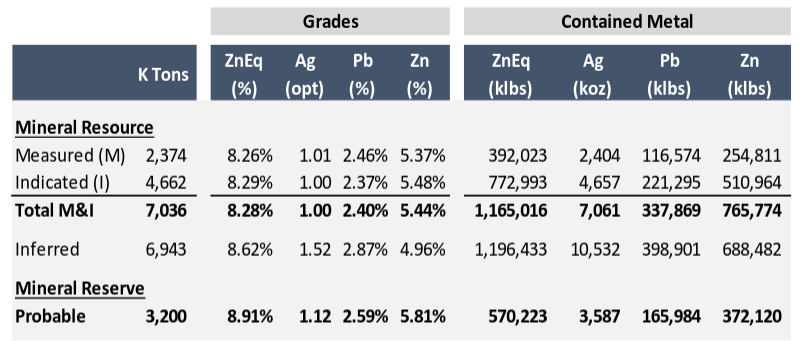

Anchored by a sizeable mineral reserve, the current mine plan is based on a 100% conversion of M&I resources, and a 75% conversion of inferred resources. I believe this is reasonable, given Bunker Hill’s long history of reserve replacement throughout its operational history. The current resource stands as:

Figure 1: Bunker Hill Mine: NI-43-101 Resource

Other fundamental advantages of Bunker Hill include: cheap grid power, highway access to smelter, no union, and an operating water treatment plant with significant excess capacity.

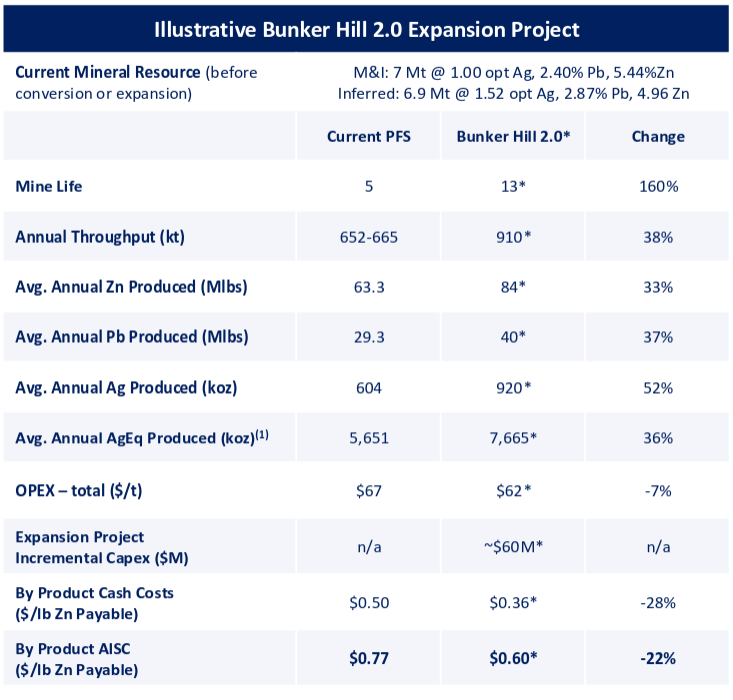

Bunker 2.0 should substantially improve project economics in every regard. U.S. $150m in support from EXIM should fast-track phase 2 of the build, resulting in a near-term cash flow expansion and de-risking through mine life extension:

Figure 2: Bunker Hill Mine: Projected Economics

Recoveries outlined by the 2022 PFS are fantastic:

84.2% silver recovery

85.10% Zinc recovery

88.20% Lead recovery

I model an initial ~1,800 tpd ore throughput, expanded to ~2,500 tpd as Bunker 2.0 is built. Stockpile grades are expected to be 1 Oz/t Ag, 5.4% Zn, and $2.46% Zn - yielding U.S. $152m of revenues, scaling up to U.S. $210m as the project expands. Annual opex is expected to range between U.S. $70m-$100m, based on company guidance. Total NSR royalties on the project sum to ~5%.

Base case NAV has been somewhat expanded by the possibility of debt refinancing at much lower interest rates. The current weighted average rate on project debt is ~10%, which could be re-financed at LIBOR + 100 bps using the debt facility pledged by EXIM. This would meaningfully reduce interest expense and increase early-stage free cash flows.

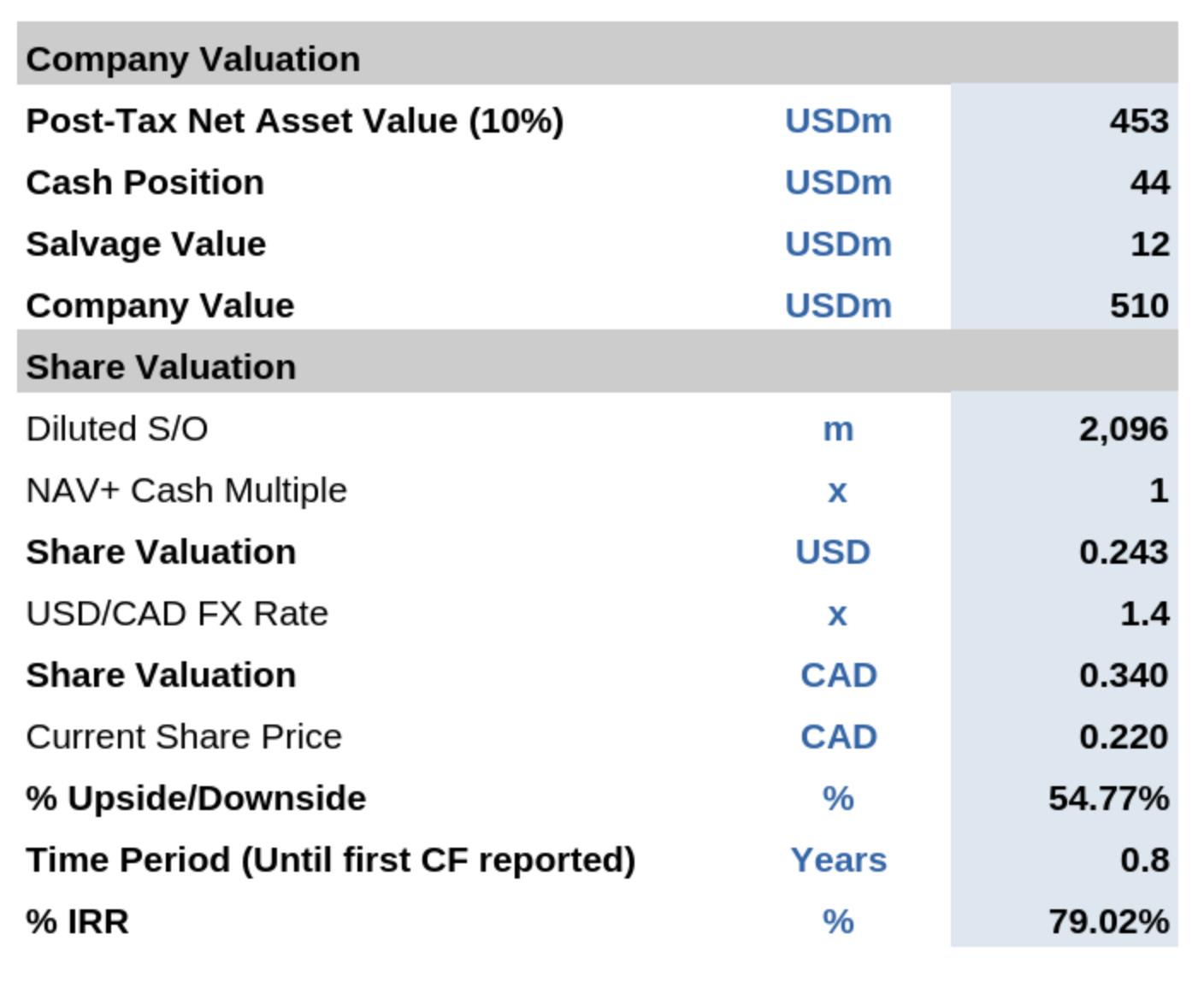

I model Net Asset Value (10% discounted, inclusive of debt repayments) to be U.S. $453m, at spot commodity prices. What does this mean for the shares? Taking into account cash, salvage value, and dilution, the mine ramp up offers shareholders an attractive 79% IRR:

Figure 3: Bunker Hill Mine: NAV-Based Valuation

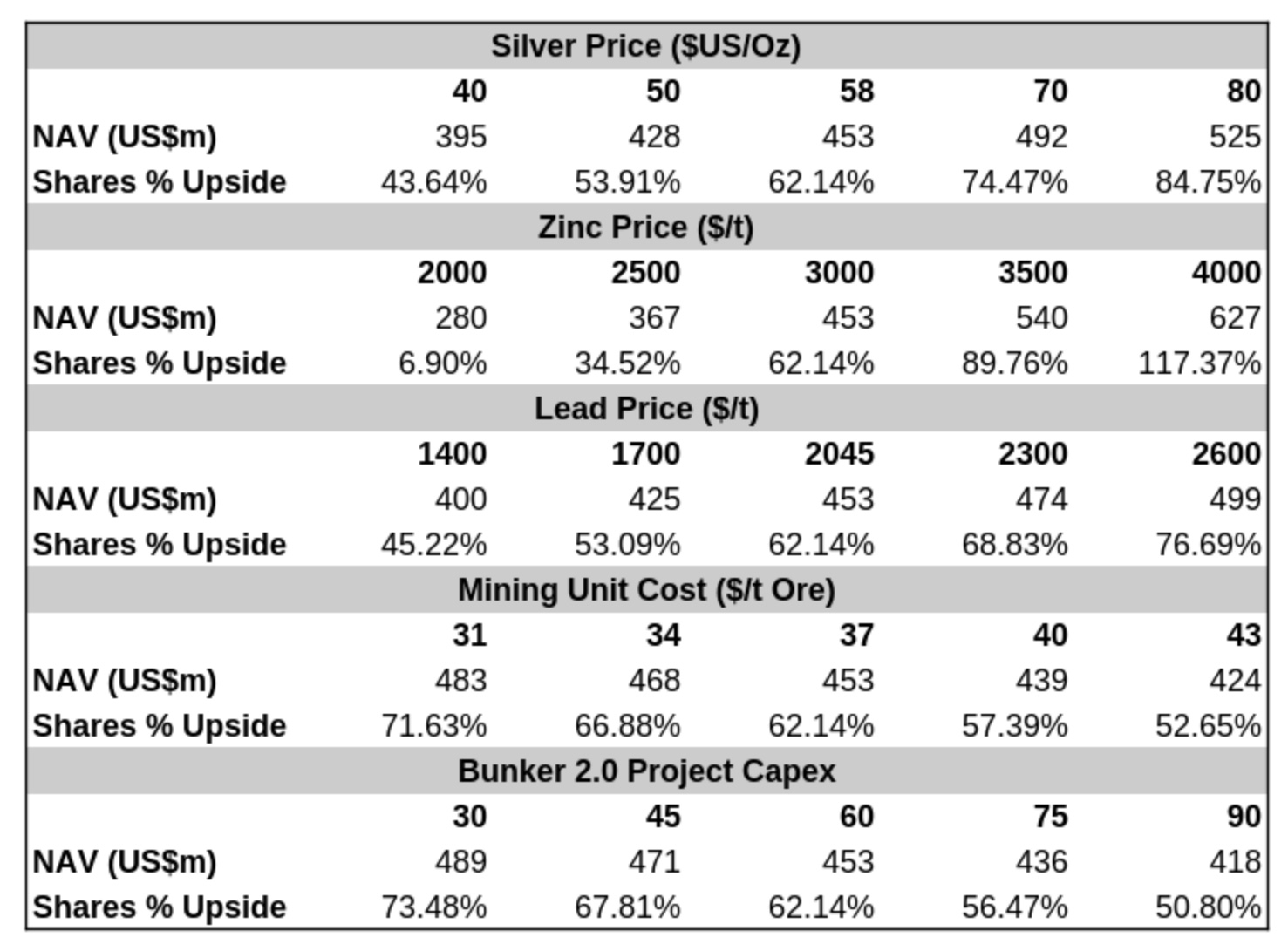

NAV is impacted by various key sensitivities, but all realistic scenarios yield at least some upside:

Figure 4: Bunker Hill Mine: Sensitivity Analysis

Overall, BNKR offers highly asymmetric exposure to Silver, Zinc, and Lead, without most of the risk of a typical junior. Bunker Hill is a pre-existing mine with a long production history, construction execution risk has been almost entirely eliminated, and capex overrun risk has been substantially reduced.

Exploration Upside - Bunker Hill & Ranger-Page

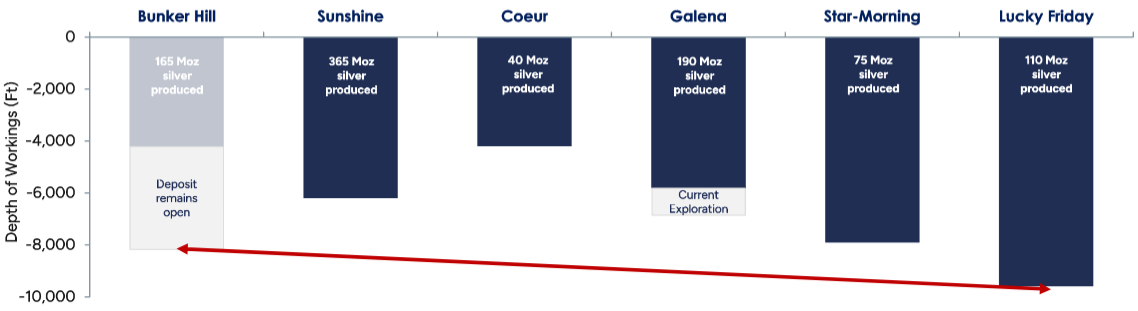

At Bunker Hill, the deposit remains open at depth. Many other mines across the same system have expanded operations to double the present maximum depth at Bunker Hill, ~4,000 ft.

Figure 5: Bunker Hill Mine: Exploration Upside

Furthermore, Bunker Hill’s recent acquisition of the Ranger-Page mine has provided the company with a “target rich environment” for exploration. Historical drilling and production from the Ranger-Page mines indicate high-grade Silver-Lead-Zinc mineralisation remains open at depth and along strike. Of the 6 historic mines on site, 4 mined to a depth of less than 61m, meaning significant potential for open-ended exploration, given the context of several 6-8,000m depth mines in the local area. The Ranger-Page property has historically produced 1.1b lbs lead-zinc and 14.6Moz of silver. In addition, the Ranger-Page acquisition could also aid exploration at Bunker Hill, with the existing underground workings at Ranger-Page providing exploration access to deeper levels of the Bunker Hill system.

“The Silver Gap” - the area on the border between Ranger-Page and Bunker Hill, also remains largely unexplored. Overall, there is plenty of exploration upside here. Whilst I don’t price it into my base case, the optionality for a multi-bagger here is certainly there.

The BNKR Management Team

Mr. Richard Williams (Executive Chairman) has an established track record of value creation, pioneering and leadership within the mining industry and various other challenging assignments. Mr. Williams has previously served as the COO of Barrick Gold, CEO of an African and Central Asian-focused exploration business, and the Commanding Officer of the United Kingdom Special Forces Regiment - 22 SAS. He is a former non-Executive Director of Trevali Mining Corporation and Gem Diamonds PLC. Mr. Richards holds a Bachelor of Science in Economics from University College London; a Master of Arts in Security Studies from Kings College London; and his MBA from Cranfield University.

Sam Ash (CEO & Director) is a former Executive General Manager of Barrick Gold’s Lumwana copper mine in Zambia. During his tenure at Lumwana Mr. Ash Delivered over $100M in sustainable free cash flow improvements, achieved 50% improvement in safety performance, executed a training and development program achieving 96% local workforce, and progressed expansion plans that doubled the value of mine. He holds a B.Eng. Mining Engineering from University of Missouri Rolla; MA in Strategic Leadership, London Business School.

Source: Red Cloud Securities

Overall, I believe management to be highly competent and experienced. The management are largely residential, with the CEO living a 30 minute walk from site. I think the project, and shareholders, are in safe hands as the final stages of the initial build are executed. You can watch an interview with Mr. Williams here:

Ownership & Capital Structure

The one thing I will openly say I don’t like about Bunker Hill is the capital structure:

Basic S/O: 1,370m

Warrants (avg C$0.22 strike): 681m

Options (avg C$0.12 strike): 30m

RSUs: 12m

Having ~50% of basic share count of ITM warrants is not ideal. However, If these are exercised today, the company would net C$150m in cash - something which isn’t priced into my valuation. Whilst it isn’t ideal - I still see the value here. My valuation is based on a fully diluted share count.

The company has a favourable shareholder base:

Teck Resources ~ 32%

Retail ~29%

Sprott Resource Streaming & Royalty ~19%

Institutions ~14%

Management & Directors ~6%

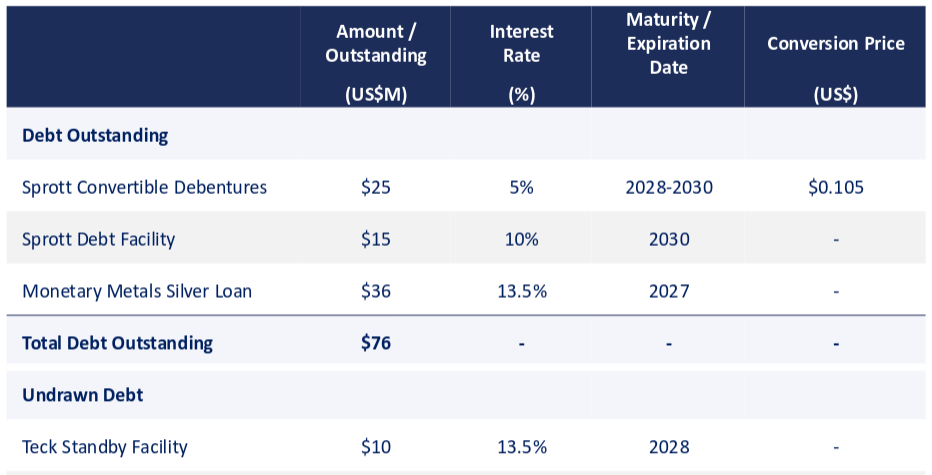

The debt stack is already fairly low yield for a mining project:

Figure 6: BNKR: Debt Capital Overview

As previously mentioned, this debt will likely be refinanced and replaced with an EXIM loan which will yield 2-5% over the LOM.

Risks

Commodity Price Risk: Downward volatility in Zinc & Silver prices would result in a materially lower NAV - $2,000 Zn yields just ~6% upside for the shares.

Capex Overrun Risk: The Bunker 2.0 cost estimate hasn’t been backed up by a technical report/feasibility study.

Dilutive Financings: Multiple private placements were closed in 2025 which priced units including a full warrant at less than the market common share price. Whilst this shouldn’t continue as the mine begins to produce cash flows, it is still a risk given the repeated history.

Catalysts

An uplisting to the NYSE - something which will bring attention to the stock, and inclusion in some indexes.

First cash flows will draw attention - analysts searching for stocks that appear cheap on a FCF yield basis will begin to find the company through screeners.

Expanded analyst coverage - currently only one analyst covers the company.

First payment of dividends - this will result in systematic buying from dividend index funds.

Discovery of additional resources at the Bunker Hill site, or at the newly acquired Ranger-Page property. A revised MRE is expected at some point in 2026.

Debt re-financing through the EXIM loan facility would expand realised NAV - causing the stock to trade at a cheaper P/NAV multiple.

A great debunking! Hopefully it won't be the hill you die on haha

Great work here, thank you for the write up.